Main Features

- ČEZ Group turnover totaled CZK 84.8 bn, which is CZK 29.2 bn higher than in the previous year due to a significant enlargement of the Group as well as higher electricity sales both in the Czech Republic and abroad.

- ČEZ Group total electricity generation amounted to 61.4 TWh; the bulk of this figure consisted of generation in fossil power stations (55.9%) and in nuclear power stations (42.1%).

- The main reasons for significant decrease of profit compared to that previously reported in the January – September 2003 financial statements are accountancy refinements (sale of ČEPS, previously reported as profit, is now reported only in the Balance Sheet) and revised nuclear power plants’ estimated operating period (from 30 to 40 years). Growth in operating revenues in 4th quarter 2003 was in line with the same period of the previous year.

- Electricity demand in the Czech Republic reached 54.8 TWh, which represents a year-on-year increase of 2.1%.

- ČEZ’s power plants covered 61.5% of overall electricity consumption in the Czech Republic compared to 56.6% in 2002.

- ČEZ is taking part in tenders for the dominant Slovak energy producer Slovenské elektrárne, a.s. and for Bulgarian distributors.

- After the crucial change of ČEZ Group on 1 April 2003, ČEZ’s stakes in its Czech distribution companies STE, VČE and ZČE increased to 97.7% - 99.1% due to share swaps and obligatory buyouts of minority shareholders during 2003. A further boost may occur during 2004 through an option with E.ON.

- Mr. Martin Roman is the new Chairman of the Board of Directors and Chief Executive Officer as of February and April 2004, respectively. Mr. Alan Svoboda is the new member of the Board of Directors and Chief Sales Officer as of April.

Prague, April 30, 2004

| Income Statement in Accordance with International Financial Reporting Standards | December 31, 2003 | December 31, 2002 | Index 03/02 | |

|---|---|---|---|---|

| CZK m | EUR m | CZK m | ||

| Operating revenues | 84,816 | 2,617 | 55,578 | 152.6% |

| Operating expenses | 77,316 | 2,386 | 44,324 | 174.4% |

| Fuel | 14,307 | 442 | 12,894 | 111.0% |

| Purchased power and related services | 21,100 | 651 | 7,328 | 287.9% |

| Depreciation and amortization | 17,611 | 543 | 11,721 | 217.5% |

| Operating income | 7,500 | 231 | 11,254 | 66.6% |

| Other expenses (income) | 841 | 26 | -542 | -155.2% |

| Income before income taxes | 6,659 | 205 | 11,796 | 56.5% |

| Income taxes | 208 | 6 | 3,375 | 6.2% |

| Net income | 5,932 | 183 | 8,421 | 70.4% |

| Unit | December 31, 2003 | December 31, 2002 | Index 03/02 | |

| Earnings per share (EPS) | CZK | 10.0 | 14.3 | 70.3% |

| Price/earnings ratio (P/E) | 1 | 14.5 | 6.5 | 224.1% |

| Return on equity (ROE) net | % | 4.0 | 6.0 | 67.3% |

| Return on total assets (ROA) net | % | 2.3 | 3.7 | 64.2% |

| Assets turnover | 1 | 0.34 | 0.24 | 139.0% |

| Total indebtedness (provisions excluded) | % | 28.4 | 26.7 | 106.5% |

| Long-term indebtedness | % | 11.3 | 15.4 | 73.2% |

Revenues, Expenses, Income

Establishment of the new ČEZ Group on 1 April 2003 makes year-on-year data difficult to compare. The consolidated unit of the new ČEZ Group for January – December 2003 contains 33 companies (ČEZ, 22 fully consolidated and 10 consolidated by the equity method), while the consolidated unit for January – December 2002 comprised only 3 fully consolidated companies and 1 consolidated by the equity method. For further details see https://www.cez.cz/en/home.html.

ČEZ Group turnover totaled CZK 84.8 bn, which is CZK 29.2 bn higher than in 2002, mainly due to enlargement of the Group (including sales of electricity by distributors to final consumers) as well as higher electricity sales in the liberalized whole sale market.

Net income, at CZK 5.9 bn, decreased by CZK 2.5 bn (29.6%) in comparison with 2002, as a result of lower EBIT by CZK 3.8 bn and higher excess of other expenses over other income (y-o-y increase of CZK 1.4 bn), all of which was not entirely compensated by lower income tax (by CZK 3.2 bn only). Operating expenses increased by CZK 33.0 bn (74.4%) to CZK 77.3 bn, mainly as a result of the Group's enlargement (regional distributors’ activities are newly included), which drove up energy purchases by CZK 13.8 bn (188%), labor costs by CZK 4.1 bn (107%) and depreciation & amortization as well. Another explanation of higher operating expenses can be found in the start of Temelín Nuclear Power Station commercial operation (Unit One in June 2002 and Unit Two in April 2003) – resulting in growth of depreciation and amortization by CZK 2.8 bn - as well as the planned extension of nuclear power plant operation from 30 to 40 years. This step, together with a newly revised estimate of nuclear decommissioning costs, caused y-o-y increase of nuclear provisions by CZK 3.5 bn. The rise in electricity generation drove up fuel costs.Other expenses amounted to CZK 0.8 bn, up CZK 1.4 bn from 2002. Income from associates rose by CZK 0.6 bn (114%). Interest on debt grew by CZK 1.2 bn due to a fall in capitalized interest resulting from Temelín’s entering commercial operation. Income tax (CZK 0.2 bn) was lower by CZK 3.2 bn (93.8%) due to decrease of net income and deferred tax.

There are two main reasons for the significant decrease in profit as opposed to that previously reported in the January – September 2003 financial statements. The first one is an accountancy refinement – the gain previously reported on the ČEPS sale (CZK 10.8 bn) is now included in balance sheet only as an effect of sale recognized in equity (CZK 7.2 bn). The second reason is the revision of nuclear power plant estimated operation period (resulting in higher nuclear provisions).

Earnings per share fell by almost 30%, in line with the decrease in net income.

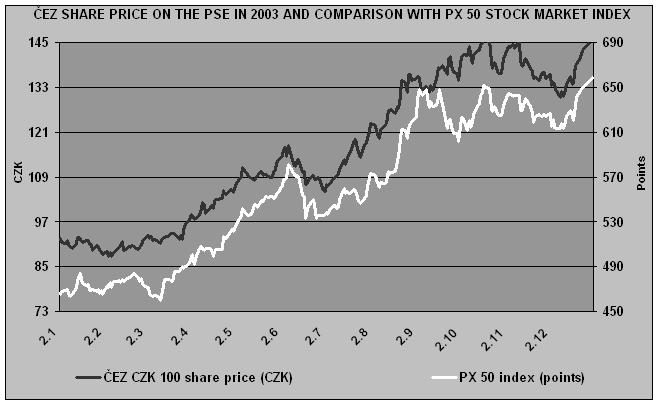

The price/earnings ratio increased from 6.5 to 14.5 thanks to a strong rise in ČEZ’s share price. The net return on equity decreased from 6.0% to 4.0% due to lower net income while shareholders’ equity remained almost unchanged. The net return on total assets decreased from 3.7% to 2.3% as a result of the lower net income and an increase in the average value of total assets. Assets turnover rose from 0.24 to 0.34 thanks to operating revenues rising faster than assets. Total indebtedness (provisions excluded) increased from 26.7% to 28.4%, as a result of ČEZ Group enlargement (current liabilities of distributors are included) and bills of exchange issued to pay for new acquisitions. Long-term indebtedness fell to 11.3%.

Sales of Electricity

In monetary terms, total sales of electricity, at CZK 79.5 bn,were up CZK 26.6 bn (50.3%) due to establishment of the new Group as well as higher electricity sales volume in both domestic and foreign markets.The total amount of electricity sold in the domestic market, at 48,883 GWh, was up 12,638 GWh (34.9%) over the previous year. Approximately 22.5%of this growth was secured by higher ČEZ sales, while the remainder was driven by the enlargement of ČEZ Group. ČEZ Group final customer market share (i.e. share in total supplies to final customers) reached 57.5%. Demand for electricity in the Czech Republic, amounting to 54.8 TWh, increased year-on-year by 1.1 TWh (2.1%). Industrial consumption increased by 503 GWh (1.6%). Household consumption increased by 386 GWh (2.7%) and small business consumption rose by 248 GWh (3.3%). Export of electricity, at 19,227 GWh, was up 3,219 GWh (20.1 %) over the previous year.

Investment Program and Financing

Net cash provided by operating activities increased by CZK 16.8 bn to CZK 35.8 bn (88.2%). This was mostly due to higher depreciation and amortization (CZK 5.9 bn).Total cash used in financing activities decreased by CZK 1.8 bn to CZK 5.1 bn (down 25.4%).

The total price paid by ČEZ for shares in the eight distribution companies was CZK 43.4 bn and is being financed as follows: CZK 15.2 bn represents the (new) valuation of the sold stake in ČEPS, CZK 5.2 bn represents sold stakes in JČE and JME, and CZK 8.0 bn was paid in cash (CZK 4.5 bn of which was for obligatory buyouts). For the remaining CZK 15 bn, four bills of exchange were issued, two of which have already been repaid, and the remaining two will be repaid in the first half of 2004.

The fifth bond issue (issue date: June 27, 1996) was replaced by the ninth issue in June 2003 at much more advantageous interest conditions. The new issue amounts to CZK 3 bn, bears interest at a fixed rate of 3.35% p.a., and matures in 2008. The eighth bond issue (issue date: June 7, 1999) will mature in June 2004. A new issue of bonds denominated in EUR is planned in 2004.

Proceeds from borrowings increased by CZK 22.8 bn to CZK 31.3 bn. Payments of borrowings increased by CZK 19.9 bn to CZK 33.7 bn.

Current credit rating for ČEZ:

| from Moody’s | 'Baa1' with a stable outlook, |

| from Standard & Poor’s | 'BBB+' with a stable outlook (change from positive to stable outlook in November 2003, the main reason being risk connected with planned expansion of ČEZ Group to other Central and East European countries) |

Other information

The contemporary ČEZ Group was established on 1 April 2003. ČEZ Group is a significant Central European utility and the tenth biggest in Europe. The favorable impact of its establishment was felt by households dwelling in the service areas of ČEZ Group’s distribution companies, where electricity became cheaper effective 1 October 2003. Synergies are expected to be leveraged in the coming years as an outcome of the regional power companies integration project, the main goal of which is to improve efficiency and accelerate the decision making process.

ČEZ was required to offer to buy out minority shareholders of ZČE and STE in June, resulting in the acquisition of a significant portion of these shares. Subsequently, ČEZ and E.ON signed transaction contractual documents on a share swap, on the basis of which ČEZ acquired E.ON’s shares in VČE and ZČE in exchange for its shares in JME and JČE. The shares were swapped and the difference in their values was settled on 30 September 2003. In connection with the share swap, ČEZ offered to buy out the minority shareholders of ZČE and VČE in September and October. This transaction brought ČEZ’s share in STE, VČE and ZČE up to the level of 97.7 – 99.1%. There is a possibility to boost ČEZ’s share in SME and SČE to 89.36% and 56.93%, respectively, using an option concluded with E.ON during 2004.

ČEZ Group is about to expand abroad. ČEZ is taking part in tenders for the dominant Slovak power producer Slovenské elektrárne, a.s. and for Bulgarian distribution companies. In the Bulgarian tender, there are 7 companies for sale divided into 3 packages, of which each private investor may acquire only one.

Mr. Martin Roman is the new Chairman of the Board of Directors and Chief Executive Officer as of February and April 2004, respectively. Mr. Alan Svoboda is the new member of the Board of Directors and Chief Sales Officer as of April.

ČEZ was recognized by Euromoney as having the best corporate governance in the Czech Republic. It is also listed in the Forbes 2000 - World’s leading companies ranking (measured by a composite of sales, profits, assets and market value) in 1125th place, which is the highest ranking of any company from the Czech Republic.

| Income Statement in accordance with International Financial Reporting Standards (IFRS) (CZK m) | Dec 31 2003 | Dec 31 2002 |

|---|---|---|

| Operating revenues | 84 816 | 55 578 |

| Sales of electricity | 79 548 | 52 938 |

| Heat sales and other revenues | 5 268 | 2 640 |

| Operating expenses | 77 316 | 44 324 |

| Fuel | 14 307 | 12 894 |

| Purchased power and related services | 21 100 | 7 328 |

| Repairs and maintenance | 4 226 | 3 847 |

| Depreciation and amortization | 17 611 | 11 721 |

| Salaries and wages | 7 994 | 3 854 |

| Materials and supplies | 3 670 | 1 838 |

| Other operating expenses/income, net | 8 408 | 2 842 |

| Income before other expenses/income and income taxes | 7 500 | 11 254 |

| Other expenses/income | 841 | -542 |

| Interest on debt, net of capitalized int erest | 1 714 | 582 |

| Interest on nuclear provisions | 1 680 | 1 532 |

| Interest income | -319 | -149 |

| Foreign exchange rate losses/gains, net | -1 915 | -3 340 |

| Gain on sale of subsidiary | ||

| Other expenses/income, net | 744 | 1 330 |

| Income from associates | -1 063 | -497 |

| Income before income taxes | 6 659 | 11 796 |

| Income taxes | 208 | 3 375 |

| Income after income taxes | 6 451 | 8 421 |

| Minority interests | 519 | |

| Net income | 5 932 | 8 421 |

| Cash Flow in accordance with International Financial Reporting Standards (IFRS) (CZK m) | Dec 31 2003 | Dec 31 2002 |

|---|---|---|

| Cash and cash equivalents at beginning of period | 4 225 | 2 280 |

| Effect of change in group structure on opening balance of cash and cash equivalents | 166 | |

| Operating activities: | 35 760 | 19 001 |

| - Income before income taxes | 6 659 | 11 796 |

| - Depreciation and amortization and asset write-offs | 17 619 | 11 735 |

| - Amortization of nuclear fuel | 3 484 | 2 071 |

| - Foreign exchange rate loss (gain) | -1 915 | -3 340 |

| - Provision for nuclear decommissioning and fuel storage | 3 656 | 641 |

| - Changes in assets and liabilities | 5 790 | 125 |

| Investing activities | -30 930 | -9 935 |

| Financing activities | -5 148 | -6 902 |

| Net effect of currency translation on cash | -59 | -219 |

| Cash and cash equivalents at end of period | 4 014 | 4 225 |

| Dec 31 2003 | Dec 31 2002 | |

| ČEZ Group electricity supplied from power plants (GWh) | 56 717 | 49 946 |

| Electricity sold by ČEZ Group in the Czech Republic (GWh) | 48 883 | 36 245 |

| ČEZ Group electricity exports (GWh) | 19 227 | 16 008 |

| ČEZ Group electricity imports (GWh) | 24 | 417 |

| Capacity, Employees | Dec 31 2003 | Dec 31 2002 |

| ČEZ Group installed capacity (MW) | 12 297 | 11 146 |

| ČEZ Group number of employees (pers) | 18 100 | 7 677 |

Retained earnings

| Balance Sheet in accordance with International Financial Reporting Standards (IFRS) (CZK m) | Dec 31 2003 | Dec 31 2002 |

|---|---|---|

| Assets | 274 143 | 231 465 |

| Fixed assets | 254 443 | 216 204 |

| Plant in service | 363 165 | 242 338 |

| Less accumulated provision for depreciation | 150 426 | 103 355 |

| Net plant in service | 212 739 | 138 983 |

| Nuclear fuel, at amortized cost | 9 574 | 7 931 |

| Construction work in progress | 10 204 | 56 513 |

| Investment in associates | 10 999 | 5 880 |

| Investments and other financial assets, net | 8 642 | 5 723 |

| Intangible assets, net | 1 997 | 1 174 |

| Deferred tax assets | 288 | |

| Current assets | 19 700 | 15 261 |

| Cash and cash equivalents | 4 014 | 4 225 |

| Receivables, net | 7 063 | 4 040 |

| Income tax receivable | 103 | 1 994 |

| Materials and supplies, net | 3 242 | 2 467 |

| Fossil fuel stock | 979 | 618 |

| Other current assets | 4 299 | 1 917 |

| Shareholders' equity and liabilities | 274 143 | 231 465 |

| Shareholders' equity | 149 687 | 143 675 |

| Stated capital | 59 152 | 59 041 |

| 90 535 | 84 634 | |

| Minority interests | 7 893 | |

| Long-term liabilities | 59 486 | 59 595 |

| Long-term debt, net of current portion | 30 965 | 35 729 |

| Accumulated provision for nuclear decommissioning and fuel storage | 28 164 | 23 866 |

| Other long-term liabilities | 357 | |

| Deferred taxes liability | 14 721 | 12 541 |

| Current liabilities | 42 356 | 15 654 |

| Short-term loans | 2 320 | |

| Current portion of long-term debt | 5 691 | 4 235 |

| Trade and other payables | 20 578 | 8 934 |

| Income tax payable | 3 203 | 256 |

| Accrued liabilities | 10 564 | 2 229 |

| Consolidated Statement of Shareholders' Equity in accordance with IFRS (CZK m) | Stated Capital | Translation Differences | Fair Value and Other Reserves | Retained Earnings | Total Equity |

|---|---|---|---|---|---|

| December 31, 2001 | 59 050 | - | - | 77 676 | 136 726 |

| Net Income - 2002 | - | - | - | 8 421 | 8 421 |

| Additional paid-in capital | 12 | - | - | 12 | |

| Acquisition of treasury shares | -181 | - | - | -181 | |

| Sale of treasury shares | 160 | - | - | 17 | 177 |

| Dividends declared | - | - | -1 480 | -1 480 | |

| December 31, 2002, as previously reported | 59 041 | - | - | 84 634 | 143 675 |

| Change in accounting policy - effect of | - | - | |||

| change in group structure | - | - | 609 | 609 | |

| January 1, 2003, as restated | 59 041 | - | - | 85 243 | 144 284 |

| Net Income - 2003 | - | - | - | 5 932 | 5 932 |

| Change in fair value of available-for-sale | - | - | - | - | - |

| financial assets recognized in equity | - | - | -101 | - | -101 |

| Gain on sale of subsidiary ČEPS, net of tax | - | - | - | 7 162 | 7 162 |

| Effect of acquisition of REAS on equity | - | -5 023 | -5 023 | ||

| Sale of treasury shares | 111 | - | - | -5 | 106 |

| Dividends declared | - | - | - | -2 657 | -2 657 |

| Returned dividends on treasury shares | - | - | - | 4 | 4 |

| Share options | - | - | 21 | - | 21 |

| Share in equity movements of associates | - | - | - | -25 | -25 |

| Other movements | - | 1 | -1 | -16 | -16 |

| December 31, 2003 | 59 152 | 1 | -81 | 90 615 | 149 687 |

This report is based on audited financial figures.